Introduction: Why This Question Matters Now

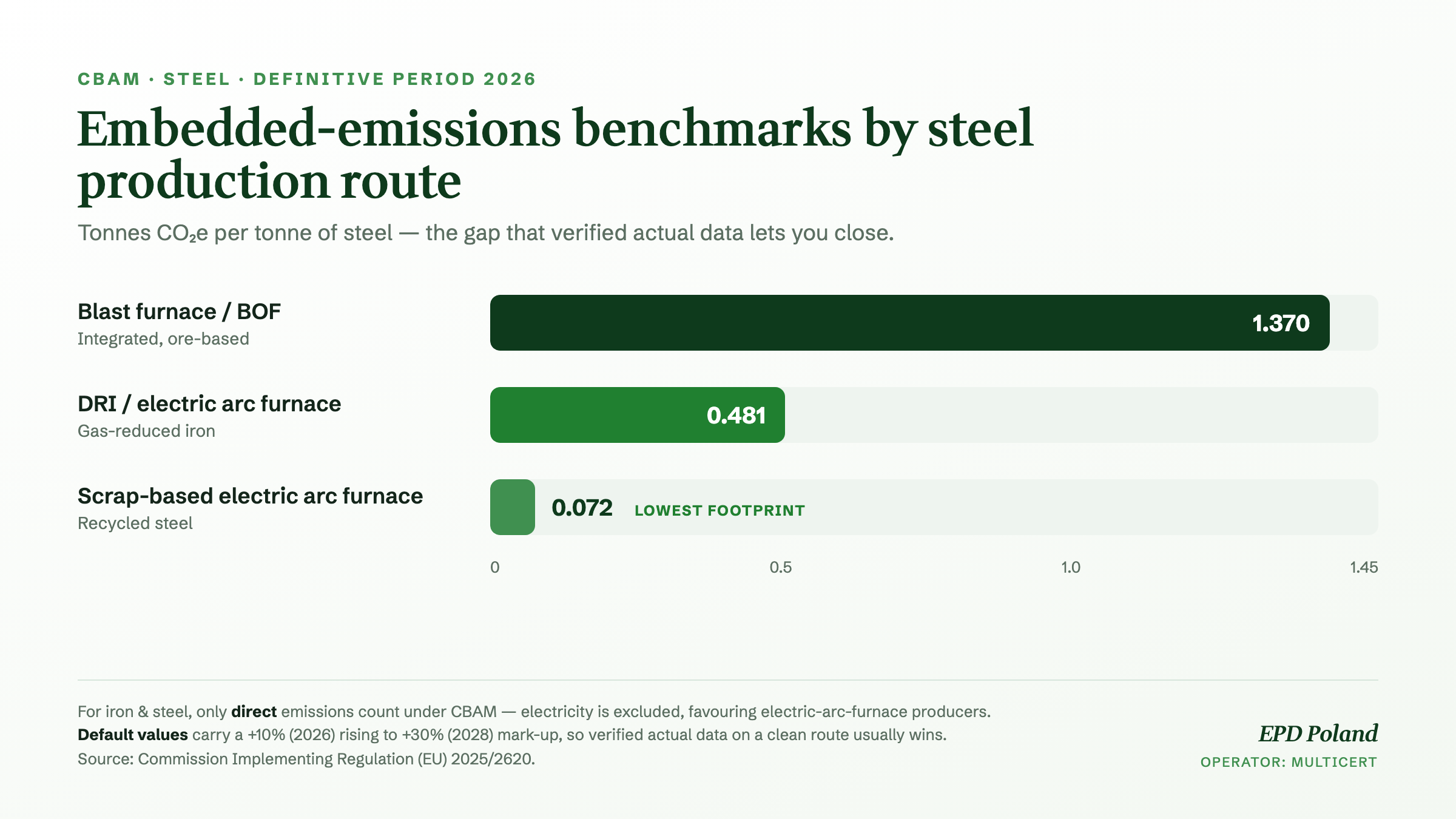

The CBAM steel benchmark ranges from 0.072 tCO₂e per tonne for scrap-based electric arc furnace to 1.370 for blast furnace. For low-carbon producers, the gap between verified actual data and the default value is the whole game.

An Environmental Product Declaration (EPD) does not satisfy the EU Carbon Border Adjustment Mechanism (CBAM), and the carbon figure in an EPD is not a CBAM emissions value. The two are built from much of the same primary data, but they differ in scope, calculation method, and verification regime.

For most manufacturers — especially low-carbon steel producers — the decisive question is not “should we publish an EPD?” but “do our verified actual emissions beat the EU default value?” This article explains how CBAM works in 2026, how an EPD relates to it, where the two genuinely overlap, and the exact steps to prepare — with references to the primary legislation throughout.

Key Definitions

CBAM — the EU Carbon Border Adjustment Mechanism, established by Regulation (EU) 2023/956. A carbon price on the embedded emissions of certain imported goods, designed to mirror the carbon cost borne by EU producers under the EU Emissions Trading System (ETS).

Embedded emissions — the greenhouse gas emissions released during the production of a good, calculated at installation level under the CBAM methodology (Annex IV of Reg. (EU) 2023/956) and expressed per tonne of product.

EPD — a Type III Environmental Product Declaration under ISO 14025 and, for construction products, EN 15804. A multi-indicator, life-cycle-based, third-party verified statement of a product’s environmental performance.

CBAM in 2026: What Is Actually Required

CBAM entered its definitive period on 1 January 2026, after a transitional reporting-only phase that ran from October 2023 under Implementing Regulation (EU) 2023/1773. The financial obligation now applies.

The operating framework was finalised in a package of implementing and delegated acts adopted in December 2025 (core implementing acts (EU) 2025/2546–2550 dated 10 December, with further acts dated 16 December; see the DG TAXUD legislation page). Binding default values were set in Implementing Regulation (EU) 2025/2621 of 16 December 2025 (published in the OJ on 31 December 2025), and the benchmarks in Implementing Regulation (EU) 2025/2620. The 2025 CBAM Omnibus simplification (Regulation (EU) 2025/2083), in force from 20 October 2025, shaped the current timetable.

Key Dates

| Milestone | Date |

|---|---|

| Definitive period begins (financial obligation) | 1 January 2026 |

| Accredited verifiers gain CBAM Registry access | from 30 September 2026 (per DG TAXUD) |

| CBAM certificate sales open | 1 February 2027 |

| First annual declaration and certificate surrender (for 2026 imports) | 30 September 2027 |

Who is liable. The CBAM obligation sits with the authorised EU importer (declarant), not the non-EU producer. A manufacturer outside the EU has no direct CBAM filing — but the emissions data it provides determines whether its EU customers can claim actual values or must fall back on punitive default values. For a non-EU producer, CBAM is a competitiveness matter, not a direct tax.

The 50-tonne exemption. Importers whose combined annual net imports of covered goods stay below 50 tonnes are fully exempt. The Commission estimates this removes around 90% of importers while retaining roughly 99% of embedded emissions.

The Point Most Guides Get Wrong: For Steel, Only Direct Emissions Count

Under the CBAM Regulation, iron and steel, aluminium, and hydrogen are subject to direct emissions only in the definitive period. Indirect emissions (from purchased electricity) are taken into account for cement, fertilisers, and electricity — but not for steel.

This matters enormously for electric-arc-furnace (EAF) and scrap-based producers, who are electricity-intensive but have very low direct process emissions. Their largest carbon line — power consumption — does not inflate their CBAM figure. The result: low-carbon steel penalised by default values can look dramatically better once actual direct emissions are calculated and verified.

EPD vs CBAM Embedded Emissions: Same Primary Data, Different Output

The cradle-to-gate boundary of an EPD (modules A1–A3) is similar to CBAM’s factory-gate boundary, which is why an EPD is a strong data foundation. But the two are not interchangeable.

| Dimension | EPD (EN 15804 / ISO 14025) | CBAM embedded emissions |

|---|---|---|

| Purpose | Market-facing environmental declaration | Regulatory value for certificate settlement |

| Governing rules | ISO 14025, EN 15804, product-specific PCR | Reg. (EU) 2023/956 + 2025 implementing/delegated acts (Annex IV method) |

| Indicators | Many (GWP plus acidification, eutrophication, water use, resource use…) | Greenhouse gases only |

| Emissions scope | Full LCA scope, incl. biogenic carbon | Direct emissions (iron & steel, aluminium, hydrogen); indirect added for cement, fertilisers, electricity |

| System boundary | A1–A3 cradle-to-gate (optionally A4–D) | Production process at installation level, including precursors |

| Allocation | LCA / PCR allocation rules | CBAM-specific allocation and monitoring rules |

| Verification | EPD programme verifier under ISO 14025 | Verifier accredited by an EU/EEA National Accreditation Body (see below) |

| Materiality | Per PCR / programme | 5% of total embedded emissions, per CN code (Annex VI, Reg. 2023/956) |

The bottom line: the gases counted, the allocation mathematics, and the verification regime are different. An EPD’s GWP figure is therefore not your CBAM value, and an EPD verification is not accepted as CBAM verification. What carries across is the primary data: metered energy, material and precursor inputs, process emissions, and production volumes.

How CBAM Embedded Emissions Are Determined

- Monitoring plan. The installation defines a monitoring methodology — calculation-based (activity data × emission factors) or measurement-based (continuous measurement) — per Annex IV of Reg. (EU) 2023/956.

- System boundary and precursors. Direct process emissions are captured per production process. For complex goods, the embedded emissions of relevant precursors are carried into the final product; where a precursor comes from several installations, a weighted average applies unless a specific source is evidenced.

- Verification. An accredited CBAM verifier checks the data against a 5% materiality threshold (Annex VI) and issues a verification report.

- Transfer to the importer. The verified value is supplied to the EU declarant for use in the CBAM declaration.

Verifier accreditation. Under Article 18 of Reg. (EU) 2023/956, a CBAM verifier is accredited by an EU/EEA National Accreditation Body by one of two routes: an ETS verifier accredited under Reg. (EU) 2018/2067 extending its scope to CBAM, or a verifier accredited specifically for CBAM under EN ISO 14065 pursuant to Reg. (EC) No 765/2008 (with dedicated CBAM accreditation scopes being established). Either way, this is a regime distinct from EPD programme verification. From 2026, EU importers may only use actual data verified this way.

Default Values vs Actual Data: The Economics

Where verified actual data is unavailable, importers use default values, which are deliberately conservative and carry an escalating mark-up: +10% in 2026, +20% in 2027, +30% from 2028. For steel, the production route drives the benchmark:

| Production route | Benchmark (tCO₂e per tonne of steel) |

|---|---|

| Blast furnace / basic oxygen furnace (BF/BOF) | 1.370 |

| Direct reduced iron / electric arc furnace (DRI/EAF) | 0.481 |

| Scrap-based electric arc furnace | 0.072 |

A note on terms: the 1.370 / 0.481 / 0.072 figures above are the harmonised CBAM benchmarks (Reg. (EU) 2025/2620), used to phase out free allocation. They are not the country-specific default values (Reg. (EU) 2025/2621) — those are generally higher, carry the mark-up, and apply only when an importer has no verified data.

US-assigned default values for iron and steel have been flagged as higher than US government (ITC) estimates — meaning US producers on clean routes are over-charged if they rely on defaults. Because indirect (electricity) emissions are excluded for steel and the scrap-EAF benchmark is very low, verified actual direct emissions frequently beat the default by a wide margin. The constraint is simple: you cannot use favourable actual data unless it is verified.

Want the numbers? See our companion guide for the full cost calculation, an interactive calculator, and a country-by-country comparison of steel default values (China, India, Turkey, US): What CBAM actually costs.

Decision rule: quantify your actual direct emissions, compare to the applicable default value plus mark-up, and verify only if the gap justifies it. For most low-carbon producers, it does.

Where an EPD Genuinely Helps — and Where It Does Not

An EPD helps by: imposing the data discipline (metered energy, inputs, process emissions, production volumes) that a CBAM dataset also requires; giving EU customers a third-party-verified, cradle-to-gate credibility signal; and letting you build one primary-data inventory that feeds both the EPD and the CBAM calculation.

An EPD does not: replace the installation-level CBAM emissions calculation; count as CBAM verification; or produce a number you can drop into a CBAM declaration.

Treat the EPD as the credibility layer and the data-quality engine — not as the compliance document.

Non-EU Producers: Sharing Data Through the CBAM Registry

The CBAM Registry includes a dedicated module for Operators of Third Country Installations (O3CI), through which a non-EU producer can register its installation, upload verified emissions data once, and share it with multiple EU declarants rather than supplying each customer separately. In practice the EU declarant shares its own EORI number with the supplier (outside the Registry); the non-EU operator then discloses its installation and emissions data to that declarant. Populating this module is how a producer turns good emissions performance into a usable commercial advantage in the EU.

A Practical Roadmap

- Run a CBAM exposure screening. Establish actual direct emissions per tonne and compare to the applicable default value plus mark-up.

- Stand up installation-level monitoring under the CBAM methodology — the longest lead-time item, and independent of verifier availability.

- Build one primary-data inventory that serves both an EPD and the CBAM calculation.

- Prepare for accredited CBAM verification so you can move as soon as capacity is available (Registry access for verifiers opens from 30 September 2026).

- Register in the O3CI module and share verified data with your EU customers.

- Publish an EPD as your credibility layer for the EU market.

How EPD Polska / Multicert Can Support You

We support the data side end to end: emissions data prepared under the CBAM methodology, EPD preparation and verification, and full pre-verification readiness so that accredited CBAM verification is fast and low-risk. The formal CBAM verification statement is issued by an accredited CBAM verifier, which we coordinate with you.

If you manufacture steel — or any CBAM-covered good — and want to know whether verified actual data beats the default value for your installation, contact us for a short exposure screening.

Frequently Asked Questions

Can I use my EPD’s GWP figure as my CBAM emissions value?

No. The boundaries are similar, but the gases counted, the allocation rules, and the verification regime differ. Use the same primary data to produce a separate CBAM figure.

Is a standard EPD verification accepted for CBAM?

No. CBAM verification must be performed by a verifier accredited by an EU/EEA National Accreditation Body (Article 18, Reg. (EU) 2023/956) — distinct from EPD programme verification.

As a non-EU producer, do I have a CBAM obligation?

No direct filing. The obligation sits with your EU importer. But your verified data determines their cost and therefore your competitiveness in the EU.

Do my electricity emissions count toward CBAM for steel?

No. For iron and steel, only direct emissions are in scope in the definitive period; indirect emissions from electricity are excluded — which favours electric-arc-furnace producers.

My emissions are low — is verification worth it?

Usually yes. Default values are set high and rising; if your actual direct emissions are lower, verification typically pays for itself. But actual data cannot be used unless it is verified.

Official References

- Regulation (EU) 2023/956 establishing the CBAM — full text (EUR-Lex)

- CBAM — European Commission (DG TAXUD)

- CBAM Legislation and Guidance — DG TAXUD

- CBAM Registry and Reporting — DG TAXUD

- Implementing Regulation (EU) 2025/2621 — default values (EUR-Lex)

- Implementing Regulation (EU) 2025/2620 — benchmarks (EUR-Lex)

- CBAM Omnibus simplification (Reg. (EU) 2025/2083) — DG TAXUD

- The EU CBAM and the role of accreditation — European Accreditation